Fast Home Loan Approval For All Visa Holders

- For any visa holders in Australia

- We approve when others said “no”

- Borrow up to 95% of the purchase price

- Competitive interest rates

- No cost, no obligation service

Australian Citizens Living Overseas Please Click Here

MAP Mortgage Brokers is often contacted by Australian temporary residents (that is, foreign citizens who do not hold permanent residency) seeking a home loan to borrow over 80% of the purchase price. They have often approached their own bank and possibly one or two mortgage brokers and have been advised that their maximum lend is 80%.

MAP specialises in assisting temporary resident migrants with home loans to 95% LVR question at normal bank interest rates where they are purchasing with their Australian citizen or permanent resident partner or spouse.

MAP can also assist subclass 457, 475, 487 and 495 visa holders living and working in Australia with a 457 Visa home loan to 90% LVR and will guide you through the entire

process including FIRB approval.

If you have a deposit of 20% or more, MAP can still assist as every bank has their own individual policies, procedures and different specials on offer at different times.

If you are purchasing with an Australian Citizen / Permanent Resident and you hold either a subclass 457, 300, 309, 820, bridging visa A or B, 461 visa, or any other visa that permits you to work in Australia (excluding tourist visa’s), standard lending policy applies and 95% is available.

The minimum deposits required by Migrants on temporary provisional visas will vary depending on the subclass of visa and occupation of the holder. Effectively, some banks and non-bank lenders have determined that certain visa holders will be a satisfactory lending risk given that;

Here are some of the most common visas banks will extend mortgage finance to and the minimum deposit required:

This is not an exhaustive list and most other types of visas that permit the migrant to work in Australia will be accepted with a 20% deposit.

If purchasing with an Australian citizen or permanent resident then disregard the above and note that only a 5% deposit plus purchasing costs is required in this scenario.

Whether you are a temporary resident or not, contributing 20% plus purchasing costs to

purchasing your home may not be possible for many. Further, you may have the required funds to borrow at 80% but this would leave you limited funds in case of an emergency.

Below is an example loan scenario for a purchase of $400,000 residential property in NSW at 80% and 95%. Note that The 95% structure may not be suitable but perhaps an LVR of

85 – 90% may make a significant difference to your finances. it is worth remembering also that the LMI premium works on a sliding scale so the bigger your deposit and therefore lower the LVR, the cheaper the LMI premium will be.

Please note that the below figures are estimates only.

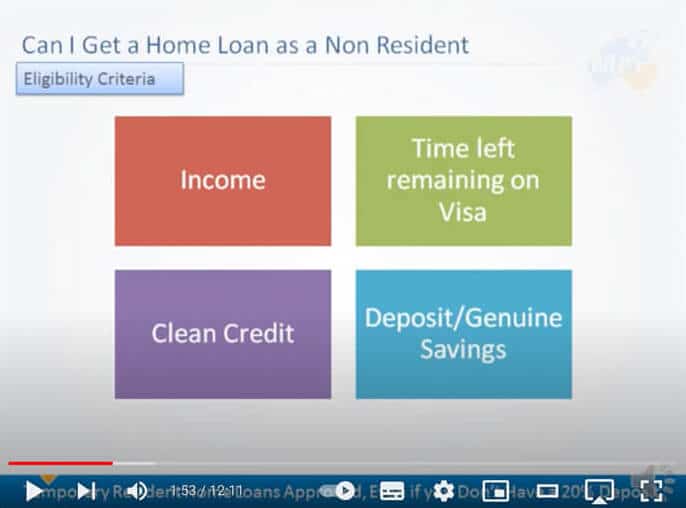

This is a short presentation by Craig Vaughan of MAP Home Loans on arranging a home loan to purchase property in Australia whilst on a temporary resident visa or as a non resident. The video covers the deposit requirements and eligibility requirements to arrange mortgage approval as well as briefly covering the steps involved in purchasing a home or investment property in Australia.

Arlyn ZHi Craig,

Thanks so much. All credits goes back to you as you helped me make all this happen.I couldn’t thank you enough for the job excellently done.

I’m glad you will still be of assistance until my house is built and I will send you a photo of the land with me and sold caption in it asap.

Cheers[Arlyn was a doctor from the Phillipines on a 457 Visa. She was on a contracting basis – that is, she got paid roughly 70% of what she billed. We assisted Arlyn with a 90% Mortgage with No Lenders Mortgage Insurance payable so she could buy a house and land package]

Request an exploratory chat about your options and how to secure fast home loan approval, at a competitive rate – even if you don’t have a 20% deposit.

Almost there, please complete the form to request your..

In this Guide, you’ll discover…

Free Report LIVE 2020 WDS

Almost there, please complete the form to request your..

In this FREE phone consultation, you’ll discover…

And, much more – We will answer any of your questions!

In this Guide, you’ll discover…

We guarantee 100% privacy. Your information will not be shared.

In this Guide, you’ll discover…

We guarantee 100% privacy. Your information will not be shared.

Almost there, please complete the form to request your..

In this Guide, you’ll discover…

In this Guide, you’ll discover…

We guarantee 100% privacy. Your information will not be shared.

We allow you to…

We guarantee 100% privacy. Your information will not be shared.

We allow you to…

We guarantee 100% privacy. Your information will not be shared.

We allow you to…

We guarantee 100% privacy. Your information will not be shared.

We allow you to…

We guarantee 100% privacy. Your information will not be shared.

Almost there: please complete the form to request your…

We respect your privacy